New arrangements for distributing GST

Introduction

In 2018, the Commonwealth Parliament legislated a new way to distribute GST revenue among the states and territories (states). This has been referred to as the new equalisation arrangements.

The key elements are:

- a new equalisation benchmark linked to the fiscally stronger of NSW or Victoria

- a GST relativity floor

- Commonwealth funded top-ups to the GST pool

- transitional arrangements, staging implementation of the new equalisation benchmark and giving states a no-worse off guarantee.

This paper briefly outlines the new arrangements.

A new equalisation benchmark

Since introducing the GST in 2000, the Commonwealth has distributed the revenue among the states. Because they have different service delivery needs and abilities to raise revenue, a different amount of GST per person is allocated to each state. It seeks to put all Australians on a level playing field in terms of their potential to access services and infrastructure. This is referred to as fiscal equalisation.

The per person GST share is expressed as a ‘GST relativity’. If all states had the same fiscal capacity, each would have a GST relativity of 1 and receive the same GST per person. Because their needs are different, fiscally stronger states have a GST relativity below 1 (and receive less than the average GST per person), and fiscally weaker states have a GST relativity above 1 (and receive more than the average GST per person).

Prior to the new approach, equalisation gave each state the fiscal capacity of the fiscally strongest state to provide services.

The new equalisation arrangements ensure that each state’s GST relativity is at least as high as the relativity of the fiscally stronger of New South Wales or Victoria (referred to as the ‘standard state’). This means no state will receive less GST per person than the standard state.

Should any state be fiscally stronger than the standard state, its GST relativity will be increased to the relativity of the standard state. Given the GST is distributed from a fixed funding pool, other states’ relativities will fall to accommodate this increase.

In practice, a state that has its relativity lifted to that of the standard state will end up with a higher fiscal capacity. The other states will have a fiscal capacity lower than the strongest state, but similar to the standard state.

A GST relativity floor

The GST floor sets a relativity below which a state’s GST share cannot fall. It creates a minimum per person GST share that each state receives, irrespective of its fiscal circumstances.

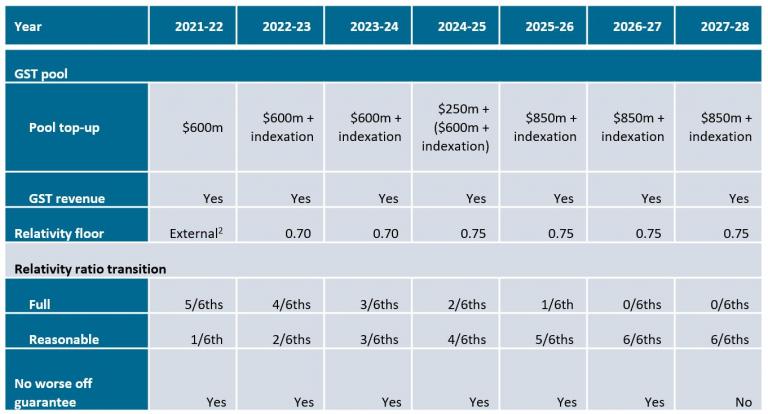

In 2022-23 and 2023-24, the floor will be 0.70. From 2024-25, the floor will increase to 0.75. If the floor is activated, it will be financed from the GST pool with Commonwealth top-ups.

While the floor will be a permanent feature of the new arrangements, it is very unlikely to be needed once the new equalisation benchmark has been fully implemented. The new benchmark is expected to provide each state with a minimum GST per person that is more than that provided by the floor.

GST pool top-up

The Commonwealth topped-up the GST pool by $600 million in 2021-21. This top-up will continue in each following year, with indexation. In 2024-25 the GST pool will be supplemented with a further $250 million with indexing of both amounts continuing in subsequent years.[1]

Transitional arrangements

The transition to the new equalisation arrangements commenced in 2021-22 and will conclude in 2026-27.

During the 6 year transition, GST relativities are a blend of the old and new arrangements. For 2021-22, each state’s GST relativity was based on 5/6 of its GST relativity under the old arrangements and 1/6 of its relativity under the new arrangements. For 2022-23, the split will be 4/6 and 2/6, and so on. By 2026-27, GST distribution will fully reflect the new equalisation benchmark.

A ‘no worse off’ guarantee operates during the transitional period. This ensures that, over the transitional period, no state will receive a lower cumulative amount of GST than it would have received under the previous arrangements. No worse-off payments are funded by the Commonwealth Government outside of the GST pool. The ‘no-worse off ‘guarantee is scheduled to expire after the transition ends in 2026‑27.

Table 1 Summary of the transition by year

1 2027-28 is the first year following the completion of the transition period.

2 The Commonwealth is directly funding the cost of the floor in 2021-22. After this, the floor will be funded from within the GST pool.

Source: Treasury Laws Amendment (Making Sure Every State and Territory Gets Their Fair Share of GST) Act 2018.

Productivity Commission Review

Under the legislation, by the end of 2026 the Productivity Commission will inquire into whether the changes to the fiscal equalisation arrangements are operating efficiently, effectively, and as intended. The inquiry will also examine the fiscal implications of the new arrangements for states.

[1] Treasury Laws Amendment (Making sure every state gets their fair share of GST) Act 2018, Section 8A.